# Leverage Traders

### [Opening/Adding Positions](https://limitless.gitbook.io/limitless/user-guide/leverage-traders/adding-and-opening-positions)

A trader can open a long position for token0/token1(token 0 longed with token1 as margin) or token1/token0(token 1 longed with token0 as margin).

**Example**: Let's assume token0 is ETH and token1 is USDC, and also assume that the current price of ETH is 2000 USDC per ETH. When a trader opens a 100x ETH/USDC long with 100USDC as his margin, the protocol will initiate the subsequent sequence of actions:

* A) From the ETH/USDC pool, the protocol will withdraw 9900 USDC worth of liquidity from (a combination of) ticks that average up to 1980 USDC/ETH or above. An example of a borrowable tick range that satisfies this condition is the 1980-1985 range([determined by an algorithm on the backend and is abstracted to traders](https://limitless.gitbook.io/limitless/advanced/determining-which-ticks-to-borrow-from)).

Borrow from liquidities outside the current tick(purple block)

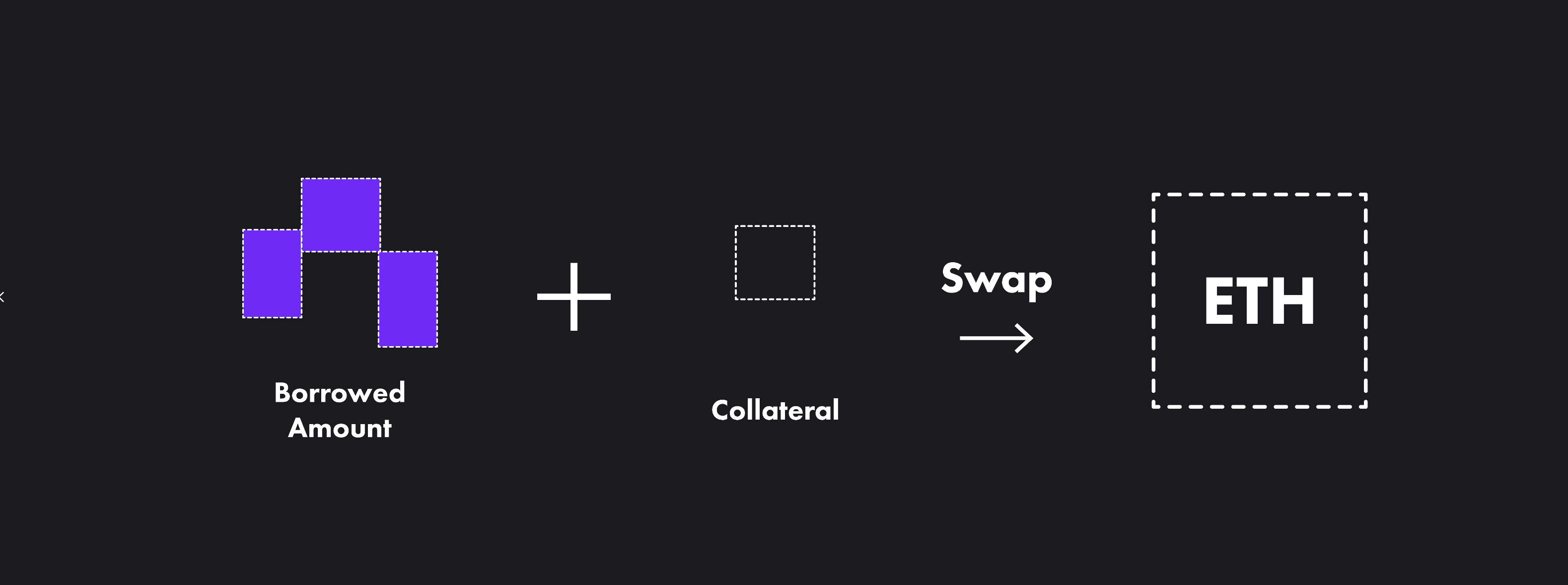

* B) Trade the borrowed 9900 USDC + 100 USDC margin = 10000 USDC to 5 ETH(ignoring slippage+fees) in the most liquid exchanges(using a dex aggregator).

Swap Borrrowed Amount + Collateral

* C) The trader now has a 100x levered 5ETH position. Note that the position is equivalent to a 9900 USDC loan collateralized by 5ETH(99% LTV).

Upon opening or adding to a position, a trader is required to pay **initial premiums** to fund their premium deposit. This deposit is then gradually depleted on a per-block basis, in line with the [premium model](https://limitless.gitbook.io/limitless/intro/premium-model).

All positions can be left open perpetually; regardless of the current price. The trader just has to regularly pay [premiums](https://limitless.gitbook.io/limitless/intro/premium-model) by replenishing the deposit.

### [Closing/Reducing Positions](https://limitless.gitbook.io/limitless/user-guide/leverage-traders/managing-positions)

A trader can reduce or close a long position for token0/token1 or token1/token0 at all prices. Doing so will repay the debt to Uniswap LPs, by providing liquidity back to the borrowed liquidity ranges.

Let's continue the example from 1). Note that the trader borrowed 9900 USDC from 1980-1985 USDC/ETH tick ranges.

The trader wants to close the 5ETH position, at potentially different prices:

### Outside borrowed range: If the Price of ETH/USDC > 1985USDC

In this instance, the protocol would simply sell 5 ETH in the most liquid exchanges(using a dex aggregator), the USDC debt would be repaid by providing liquidity back to Uniswap, and the trader would simply be entitled to his margin + PnL.

For example, when the price is 1990 UDSC per ETH, the trader can sell 5ETH for 9950 USDC. He will repay 9900USDC to the 1980-1985 ticks, and receive 50USDC back. His PnL is then Received Funds - Initial Margin = 50 - 100 = -50 USDC.

{% hint style="info" %}

**Important:** When a position is "Outside Range", the trading experience and payoff computations are equivalent to those of any other leverage trading applications.

{% endhint %}

### Inside borrowed range: If 1980USDC <= Price of ETH/USDC <= 1985USDC

In this instance, a percentage of USDC borrowed from 1980-1985 is expected to convert to ETH. [The protocol would have to sell a portion of the ETH to USDC](https://limitless.gitbook.io/limitless/intro/participants/broken-reference) to form the appropriate ratio such that it can provide liquidity back to 1980-1985. The trader would be entitled to tokens left over after repaying debt(providing liquidity back).

### Crossed borrow range: If the Price of ETH/USDC < 1980USDC

In this instance, the USDC debt in its entirety is expected to convert to ETH. (Assuming the debt is uniformly borrowed between 1980-1985 with an average price around 1982.5). The AMM expects 9900/1982.5 = 4.993 ETH, which is covered by the 5ETH. The trader will be entitled to the remaining 0.007ETH.

{% hint style="info" %}

In typical leverage trading applications, a 'Crossed Range' position often is synonymous with being liquidated. However, rather than facing forced liquidation, the trader has the option to wait until the position exits the 'Crossed Range' status, provided they continue paying premiums.

However, if the trader anticipates no reversal, they may opt to close the position to avoid further premium expenses.

{% endhint %}

#### Liquidation Free

Note that this is how the trader averts forced liquidations: by ensuring the position can be repurchased by the LP whenever it is closed, in exchange for continuous premium payments. Essentially, the LP is selling a covered call option to the trader.

### [Paying Premiums](https://limitless.gitbook.io/limitless/intro/participants/broken-reference)

Before opening any positions, the trader must deposit a certain amount of premium entitled to the position. This deposit will be deducted on a per-block basis per the premium quoted for every block.

After a position is opened, a trader will have to replenish this deposit as it tends to 0. If the deposit is fully depleted, **his position is forcibly closed.**

When the position is closed, the trader will be entitled to all unused premium deposits.

## Fees

In addition to premiums, traders are required to pay fees that consist of the following

* Loan Origination Fee(default at 0.1% of borrowed amount)

* Profit Share(default at 5% of incurred profit)

The profit share mechanism exists to compensate the LPs for their increased illiquidity risk. Traders, in return, do not suffer liquidation penalties as there are no liquidations.

### Limit Orders

Traders can also post limit add and reduce orders. Fff-chain 'filler' bots will monitor the blockchain with active limit orders, and fill them when it is profitable to do so. When an order is filled, a position is added or reduced automatically on behalf of the trader.

####